Regulatory change is rewriting the playbook for corporate social impact. In the U.S., between new tax rules, Executive Orders, shifting memos and evolving governmental support for nonprofits and DEI, leaders face a complex reality: you can’t control the policy climate, but you can control how your program evolves. The good news? Companies that adapt with clarity, care and rigor are already finding their footing.

This article distills what we’re hearing from Corporate Social Responsibility (CSR) executives in the U.S. and pairs those insights with credible sector analysis on the One Big Beautiful Bill Act (OBBBA) to offer an action framework for the preparation of the next tax year.

The rules may change but your purpose shouldn’t.

The new baseline: what changed (and why it matters)

Recent U.S. tax reforms alter both corporate and individual giving:

Corporate giving: Companies must give at least 1% of taxable income for their charitable contributions to be deductible (the 10% cap and 5-year carry-forward remain). The first 1% of taxable income given isn’t deductible — it’s simply the threshold. Only contributions above that floor qualify, and total deductions remain capped at 10% of taxable income. If giving falls below 1%, it provides no charitable tax deduction and can’t be carried forward to future years. Fidelity Charitable’s analysis of OBBBA notes that the 1% floor “changes the starting line for corporate philanthropy.”

Individual giving: A new 0.5% of Adjusted Gross Income (AGI) floor for itemized charitable deductions takes effect for tax years beginning after December 31, 2025, changing household giving incentives and year-end strategies.

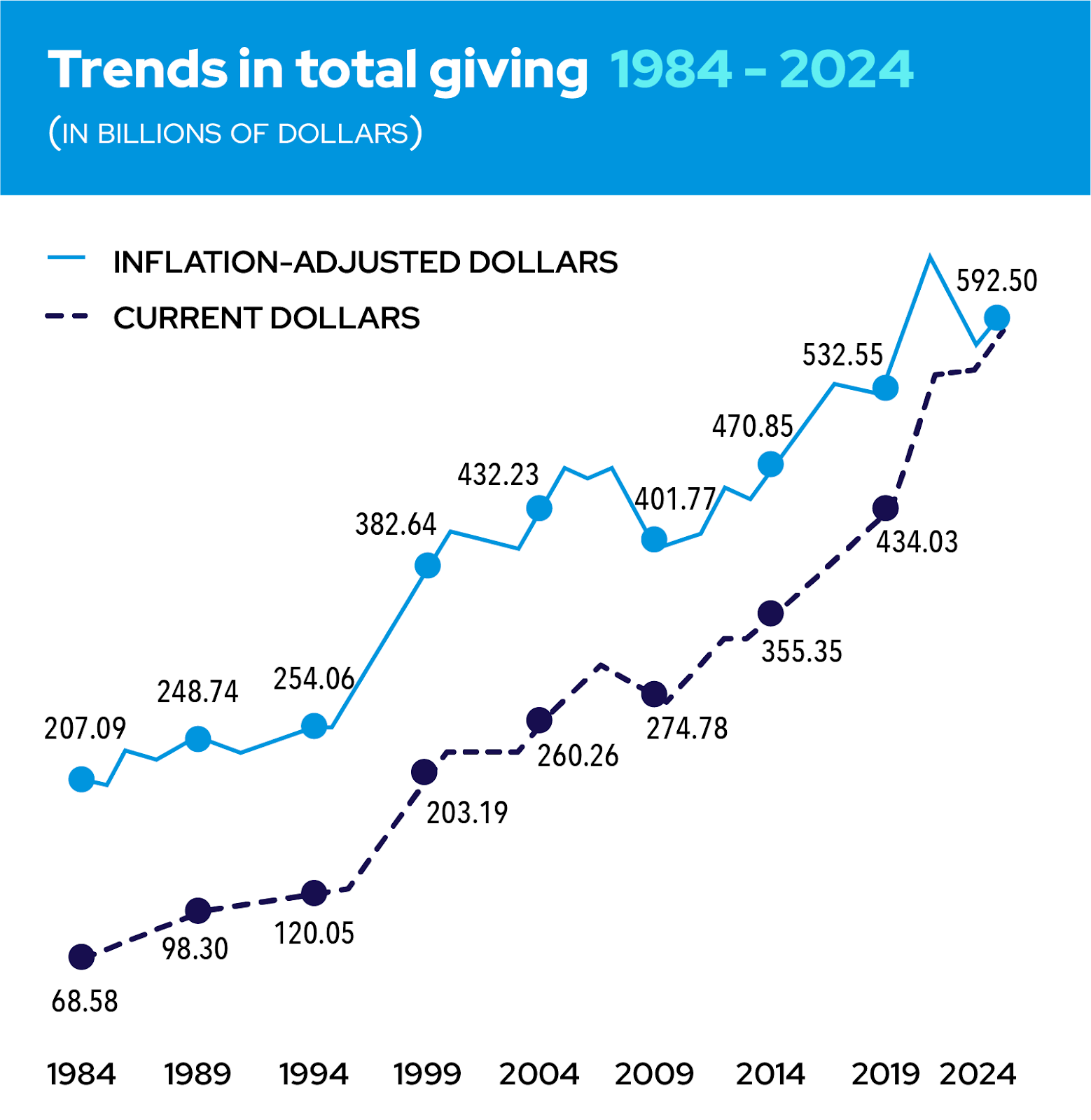

Zooming out, the philanthropic market itself remains resilient: U.S. giving rebounded in 2024 (corporate giving up mid-single digits, individual giving up as well), but nonprofits anticipate 2025 headwinds as public funding tightens and uncertainty lingers. The current policy environment is creating additional pressure on the need for forward planning around corporate giving, granting and community impact programs.

Signals to watch

Based on our data and discussions with leaders and experts in corporate social responsibility and philanthropy, here are three themes we are hearing:

- We may see more companies and individuals bringing forward donations into this year to take advantage of existing tax laws, especially if companies don’t meet the 1% threshold which goes into effect after Dec. 31, 2025.

- Longer-term, E&Y has forecasted a drop of up to $4.8B in corporate giving annually, which is a little over 10% of annual corporate giving in the USA based on GivingUSA’s 2024 data (where corporations gave $44.4B in 2024).

- Similarly, joint Independent Sector research has forecasted a $4.1 to $6B drop in individual giving, which represents a 1.5% drop in annual individual giving which was at $392B last year, according to GivingUSA.

If we see the drops that are expected here, it would amount to about 2% less in overall giving annually — this may not sound like a lot but it represents a potential $10.8B reduction in nonprofit giving.

Looking at the long-term trajectory of giving, the U.S. government has previously changed the tax structure related to giving several times over the past 40 years, and yet giving by individuals and corporations has grown at roughly a 3% Compound Annual Growth Rate (CAGR), which falls in line with US GDP. This is a counter-point to the research and data provided above. Ultimately, it proves that it’s difficult to anticipate what the effect of the new tax reform will be on corporate and individual behaviour.

A six-step playbook to stay focused

Earlier this year we shared guidance on how CSR leaders can navigate uncertainty while staying true to their corporate purpose that still holds true. When it comes to some of the U.S. tax reform implications for corporate giving and grantmaking, here are six considerations for your programs:

- Start by understanding how your company treats your charitable giving for tax purposes. Deductibility of charitable gifts as either business expenses or charitable contributions may warrant professional advice from your tax team.

- Build a single source of truth for tax-relevant rules across entities and markets that define thresholds, carry-forward rules, and approval process. Examples such as:

- Minimums (e.g., 1% corporate charitable deduction floor) and caps (10% remains),

- Eligible gift types, valuation approaches, and carry-forward logic (5 years),

- Resources (Legal, Tax/Finance, CSR, marketing) linked to clear roles & responsibility.

- This can help reduce interpretation variance and accelerate compliant decisions.

- Engage in scenario-planning. Model base / downside / upside scenarios for 2026–2027 that incorporate: the 1% corporate charitable deduction floor, revenue variability, deduction types and foundation vs. direct corporate giving.

- Optimize timing and solution for tax efficiency. Given the 0.5% of adjusted gross income (AGI) floor for itemized charitable deductions impacting individuals and the 1% corporate charitable deduction floor, timing matters. Some companies are considering front-loading gifts while others are evaluating funding Donor Advised Funds (DAFs).

- Consult tax advisors for entity-specific guidance or feel free to contact us about how our Global DAF solution could work for you.

- Continue to measure what matters. Tie activities to business-relevant outcomes with community impact (for example: program access, graduation rates, food security, talent attraction, employee engagement and retention, and skills-based volunteering hours). In uncertain climates, evidence is your budget’s best friend.

- See how this global manufacturing company demonstrates business outcomes.

- Protect employee engagement and culture. Companies that overly reduce their communications and public commitments risk eroding trust among both employees and consumers, negatively impacting their bottom line. Continue to support your teams by creating spaces and psychological safety norms through activities such as volunteering and matching campaigns, which are proven, out of 90 interventions can have a notable positive effect on well-being. Celebrate every contribution.

- See how a metal solutions company achieved 83% employee participation.

Keep your purpose steady — and your playbook agile

The purpose of corporate impact hasn’t changed. What’s changing are the rules and incentives around how you deliver it. Companies that:

- anchor in compliance and transparency,

- plan pro-actively,

- effectively collaborate across finance, tax, legal and CSR functions

. . . will not only navigate this period, they’ll earn a durable advantage as partners to their communities and stakeholders.

Sources & further reading

- Stay informed with new insights and upcoming education forums from Benevity by bookmarking our CSR resource hub

- What changed (corporate & individual rules): The Council on Foundations overview of the 1% corporate charitable deduction floor; a note from the Association of Corporate Citizenship Professionals (ACCP) on what the floor means for accounting and reporting.

- Individual giving mechanics: National Philanthropic Trust and Fidelity Charitable CPA analyses on the 0.5% AGI floor for charitable giving and timing strategies.

- Sector context: Giving USA 2025 coverage showing resilience in giving. Aggregate giving trends and policy trade offs are summarized in this The Associated Press article.

- Possible impact to giving overall: Independent Sector research with Indiana University Lilly Family School of Philanthropy shared that according to the Joint Committee on Taxation, the provision would raise $34.4 billion in tax revenue over 10 years. However, it would reduce charitable giving by at least $40 billion over the same period; likely more. Additional research from E&Y shares estimated average annual reduction in corporate charitable giving.

Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. Please consult your general counsel or tax advisor regarding your organization’s specific situation.